Treasure Fun (formerly known as Treasure NFT) positions itself as a platform for NFT trading and investment, claiming to offer lucrative high returns through so-called "AI smart trading" and algorithmic bots. Some promotional materials even mention returns of "up to 30% monthly." This article aims to analyze Treasure Fun's operational model, registration details, and its predecessor TreasureNFT's history and user feedback to uncover the risks behind it, providing a cautious reference for potential users.

What is Treasure Fun?

To understand a platform, it is crucial to see how it defines itself to the public. For Treasure Fun (and its predecessor TreasureNFT), the official information tries to outline a unique market position.

Official Claim: The First Algorithm-Based Crypto NFT Marketplace

TreasureNFT claims to be "the first-ever algorithm-based crypto NFT marketplace." By employing "algorithmic trading modes," it aims to revitalize crypto NFT assets, distinguishing itself from mainstream platforms like OpenSea and LooksRare.

The "eBay" Model in NFT?

For a simpler understanding of Treasure Fun's claimed trading foundation, you can imagine it as the "eBay" of the NFT market.

In this model, sellers (NFT holders or creators) can list their NFT products on the Treasure Fun platform for display and sale. Buyers (users or investors) can acquire these NFTs through two main methods: a fixed-price purchase set by the seller or an auction where the highest bidder wins.

Website Registration Time

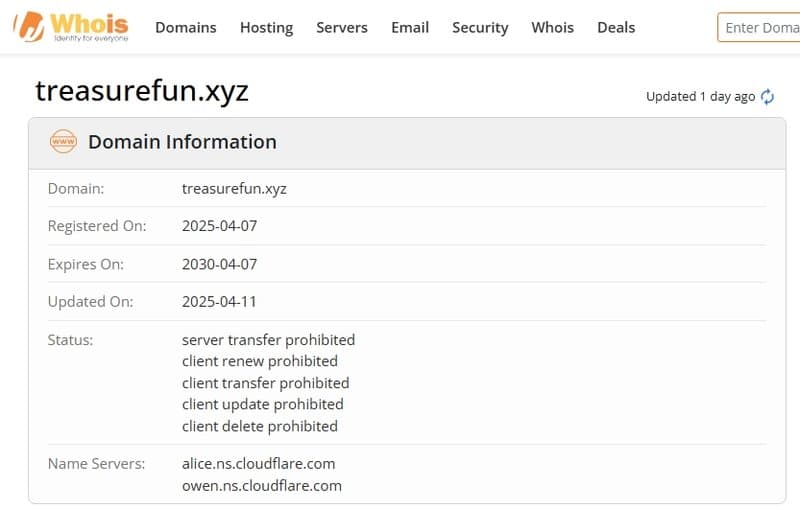

The domain name for Treasure Fun (treasurefun.xyz) is very similar to its predecessor Treasure NFT (treasurefun.xyz).

According to whois information, the Treasure Fun website was registered on April 7, 2025, indicating a very new registration date, suggesting that Treasure Fun has just rebranded and the website has only recently become operational.

Is Treasure Fun Compliant?

In the realm of digital asset investment, platform compliance is crucial for safeguarding user funds. How does Treasure Fun perform in this aspect?

Company Entity Information: Registration Does Not Equal Regulation

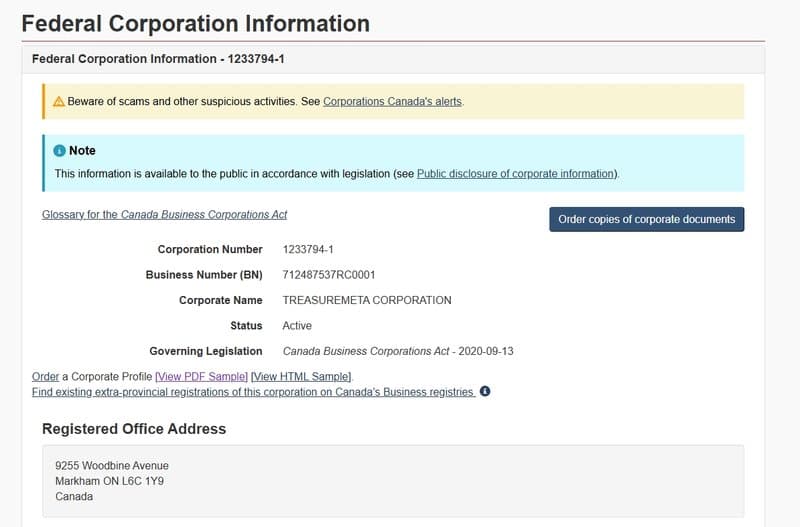

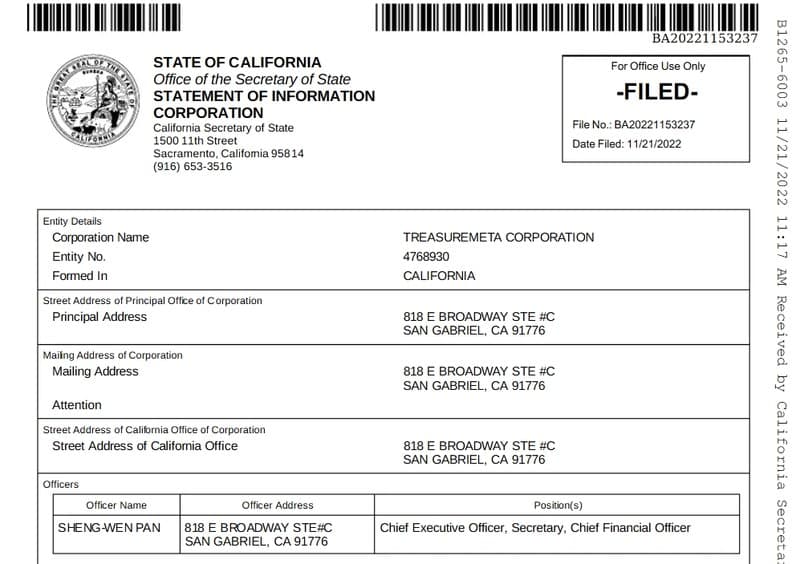

According to publicly available information, the company entity related to Treasure Fun's operations, "TREASUREMETA CORPORATION," can indeed be found in the Government of Canada's business registration system. In addition, the company name also appears in registration information in California, USA, with some details even retrievable on public document platforms like Scribd.

However, it must be emphasized that having a registered company entity is distinctly different from being under rigorous financial regulation. Company registration usually merely satisfies basic business filing requirements and does not imply that its financial services (especially those involving user investments and high-risk promises) are authorized, supervised, or guaranteed by financial regulatory bodies.

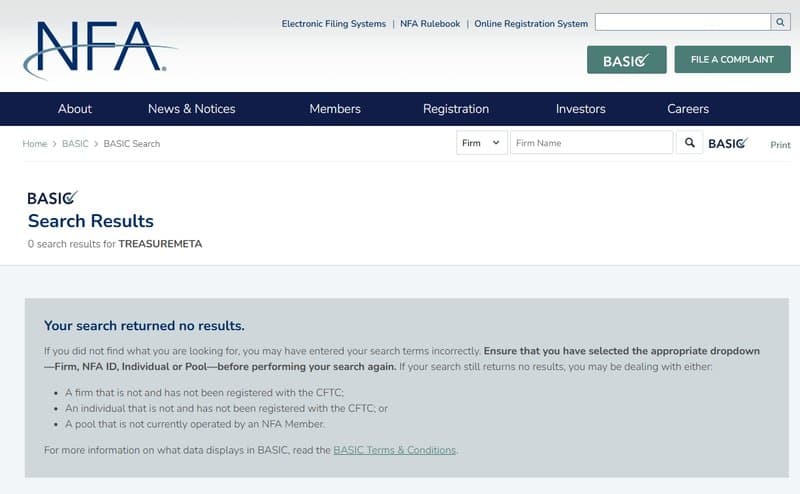

Lack of Regulation: NFA and FINTRAC Query Results

The key issue is whether Treasure Fun has obtained the necessary financial operating licenses. Queries into significant industry regulatory databases, such as the U.S. National Futures Association (NFA)—which regulates the United States derivatives markets, and the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC)—responsible for anti-money laundering and counter-terrorist financing, show no clear evidence of Treasure Fun or its affiliated company TREASUREMETA CORPORATION being regulated by these agencies.

This means that despite Treasure Fun possibly having a legal company shell, its core financial trading and investment services seem not to be under the oversight of these crucial financial regulatory bodies. For users, this points straight toward a core risk: a lack of external constraint and oversight of platform operations, making it extremely difficult to protect user rights if issues arise.

Assumptions if Treasure Fun is Regulated

Let's hypothesize that Treasure Fun has obtained some level of financial service license in a specific jurisdiction (e.g., the frequently mentioned Canadian MSB - Money Service Business license), investors must be aware of the limitations of such licenses.

For example, Canada's MSB license is typically regionally constrained, mainly focusing on anti-money laundering rather than comprehensive investor protection or assurance of business stability. However, platforms like Treasure Fun, often accessible globally, have users from every corner of the world. Thus, how can a regional, specific regulatory license ensure the safety and fraud prevention of users' funds from other global regions? The answer is evidently negative.

Moreover, according to current investigations, Treasure Fun seems unable to provide clear evidence of such basic, regional financial regulation. This undoubtedly elevates its risk level. For investors, facing a globally operated platform that lacks comprehensive regulation, investing funds is akin to placing themselves in great uncertainty.

Fake Director Registrations: Who Actually Runs Treasure Fun?

Beyond regulatory concerns, Treasure Fun's disclosures about its core operating team appear to be exceptionally mysterious, if not riddled with discrepancies.

During our company entity inquiries, a notable issue emerged:

The actual operating team of Treasure Fun is almost completely anonymous. It is challenging to find any credible information regarding the background, experience, or professional qualifications of its core team members on public internet channels. For a platform handling user funds and promising high returns, such anonymity is a huge red flag.

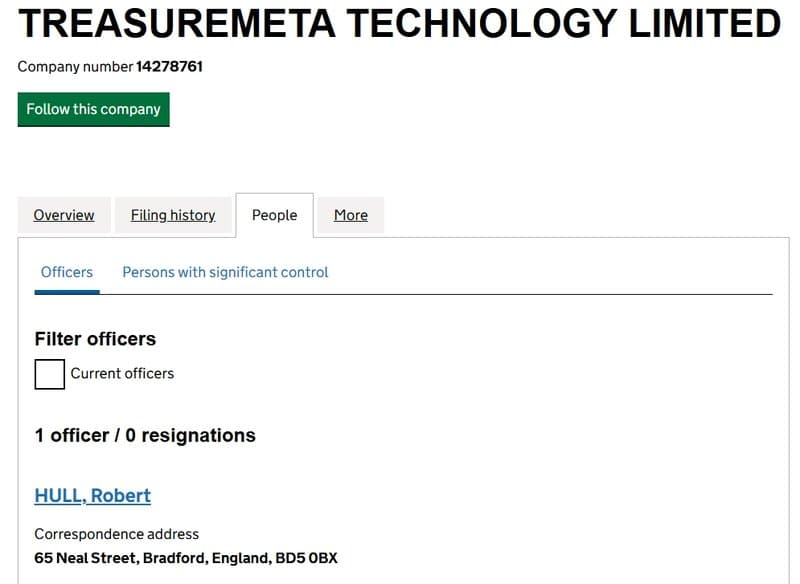

More intriguingly, even in its registered company entity information, inconsistencies and contradictions appear with its disclosed directors:

- In its predecessor TreasureNFT's registration information with the UK Companies House (which is currently invalid), the director listed is HULL, Robert.

- In TREASUREMETA CORPORATION's registration information in Canada, the director shown is VINCENT TYRONE BATES.

- For TREASUREMETA CORPORATION registered in California, USA, the director (also CEO, CFO, etc.) is SHENG-WEN PAN.

Three different registration locations reveal three entirely different director names. This situation leads one to question: what is the relation among these directors? Who is the real decision-maker and operator of Treasure Fun? The chaotic and inconsistent information makes one wonder if the platform is intentionally hiding its true controllers or team structure.

Furthermore, according to discussions and observations from some cryptocurrency enthusiasts online, Treasure Fun's team members seem to lack any public professional resume, with almost no relevant personnel found on career social platforms like LinkedIn. For a platform claiming to use "AI smart trading" and other high-tech methods, its team members are so "low-profile" and hard to trace, which contrasts sharply with the standard industry practice of striving for transparency and building trust.

In summary, the high anonymity of the operating team and the chaotic disclosure of information is a critical manifestation of the severe lack of transparency in the Treasure Fun project. Investors cannot know to whom they have entrusted their funds, nor can they assess the team's professional competence and integrity, undoubtedly pushing investment risk to the edge of uncontrollability.

Suspicion in Treasure Fun's Application and Polarized User Reviews

Beyond the grand narrative proclaimed by the platform, its application's actual performance in major stores and user feedback often reveal its true nature. With Treasure Fun, these details are equally thought-provoking.

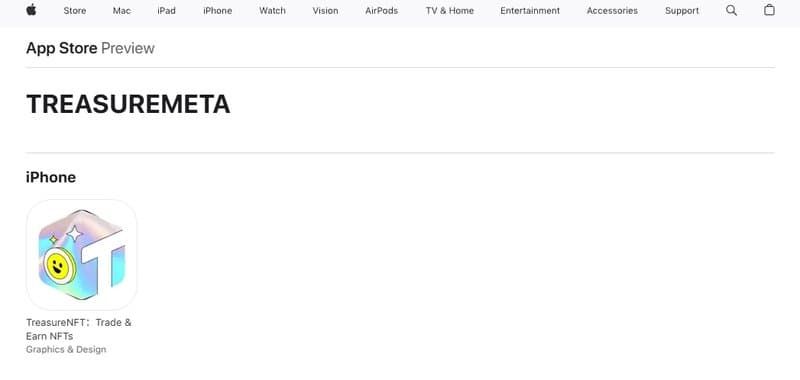

App Store "Misclassification": Why Is It Listed Under "Graphics & Design"?

A notable suspicion is that in the Apple App Store, the Treasure Fun app is not registered according to its proclaimed characteristics of NFT trading or financial investment, but is listed under "Graphics & Design."

This “misleading” classification strategy raises trust issues. Normally, financial or transaction-based applications select a matching category for accurate user searches and evaluations. Choosing an unrelated category might be to bypass stricter reviews of financial apps by the stores or to obscure its true business nature, reducing potential user vigilance. Regardless of the reason, this questions the platform's transparency and willingness to comply.

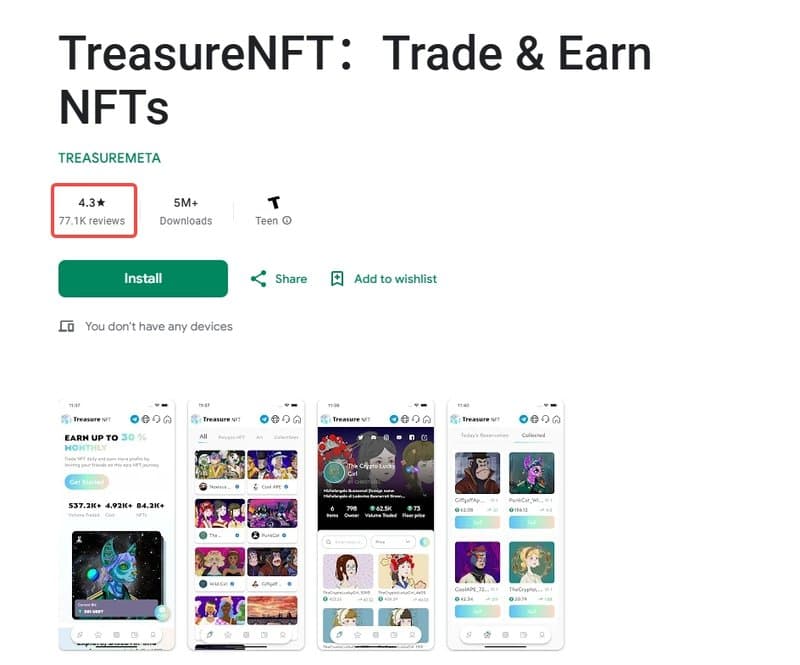

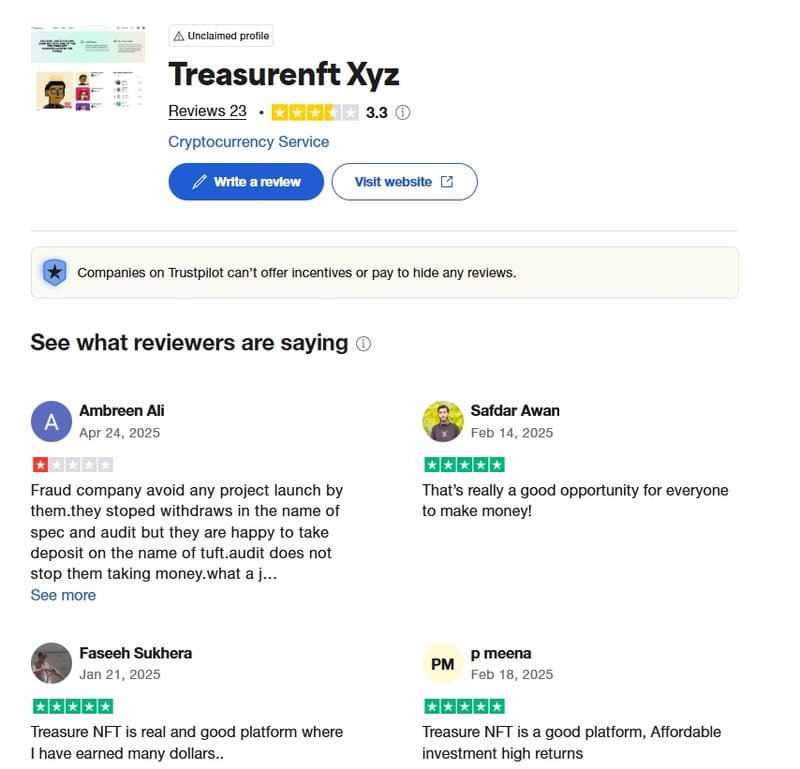

The "Polarity" of Reviews: Google Play's Manipulated Reviews and TrustPilot's Genuine Feedback

User reviews are a vital reference in determining a platform's quality, but with Treasure Fun, we observe an interesting discrepancy:

- Google Play Store: Suspected Falsely Positive Reviews? There are signs that the Treasure Fun app might have manipulated reviews in the Google Play Store. These reviews often appear hollow, lacking specific experience descriptions, contrasting with other users' genuine feedback. Such behavior of manipulating reviews aims to create a false sense of prosperity, enticing new users to download.

- TrustPilot: Detailed Negative Reviews and Uniform Positive Feedback In contrast, on third-party platforms like TrustPilot known for seeking genuine user reviews, the situation differs. Reviews here exhibit the following characteristics:

The significant contrast in reviews on different platforms, especially with TrustPilot featuring many specific and negative user feedback, strongly suggests that Treasure Fun may have serious issues in its actual operations, with user experiences and fund security far from its rosy claims. For potential users, these "hard-learned" lessons from real users are crucial risk warnings.

Treasure Fun's Astonishing Promises of Returns

In the realm of digital asset investment, high returns typically come with high risks, and the prominent display of ‘EARN UP TO 30% MONTHLY’ on Treasure Fun's app homepage unequivocally elevates its risk alert to the highest level. This is not merely an attractive number but a promise almost contradicting financial common sense.

How Unrealistic is a 30% Monthly Return?

Let's use a simple calculation to sense the "power" of a 30% monthly return. Imagine a user initially invests $1,000, achieving a 30% compound monthly return:

- After one year: The $1,000 would grow to $1,000×(1+0.30)^12≈$23,298.

- After five years: The $1,000 would balloon to an astronomical figure: $1,000×(1+0.30)^60≈$6,862,810,137,860 (over $6.86 trillion!).

From $1,000 to nearly $7 trillion in just five years. This number could purchase several of the world's top-listed companies. Such exponential growth is utterly impossible to sustain in legitimate investments in the real world.

What is the Annualized Equivalent of 30% Monthly?

If we convert a 30% monthly return into a more commonly understood annualized return (compound monthly), the effective annualized return (EAR) would be: EAR = (1+0.30)^12−1≈22.298−1=21.298, which equates to a staggering approximately 2130% annualized return!

In contrast, even top venture capital or hedge funds have long-term average annual returns far below this, with high professional thresholds and risk management. If any platform claims to provide such stable and astonishing returns to ordinary users, it almost certainly involves an unsustainable mechanism, like a Ponzi scheme—using new investors' money to pay earlier investors, until the capital chain breaks.

Conclusion

In conclusion, despite Treasure Fun (formerly TreasureNFT) cloaked in the allure of NFT trading innovation and "AI smart trading" high returns, factors such as its new website registration date, the disconnection between registered company entities and actual financial regulation, high anonymity and chaotic information of its operating team, the opaque operation of its token TUFT, suspicious categorization in the App Store, and significant real negative feedback about inability to withdraw and false advertising revealed in user reviews (particularly on platforms like Trustpilot), along with its completely unrealistic promise of "up to 30% monthly returns," jointly paint a clear picture of a high-risk investment trap. From a financial prudence perspective, the numerous characteristics exhibited by Treasure Fun are highly consistent with confirmed fraudulent investment projects, and potential investors should regard it as a highly dangerous platform, strongly advised to avoid to safeguard their financial security.