AequiSolva presents itself as a next-generation financial infrastructure platform for digital markets. On its website, it repeatedly uses slogans such as “Where Trust Is Proven, Not Promised” and highlights terms like “sub-100 microsecond matching,” “1.5M+ TPS,” “ZK-PoR,” “real-time cryptographic attestation,” and “multi-jurisdictional compliance framework.” It also describes itself as a “Financial Market Operating System” and places heavy emphasis on ideas such as verifiable trust, regulatory leadership, asset fusion, and global compliance capability.

At first glance, AequiSolva is clearly trying to create the impression that it is not just another crypto website, but a serious institutional-grade platform built for the future of finance. The problem is that strong branding is not the same as strong credibility. A company can write an impressive website, use sophisticated technical language, and surround itself with regulatory buzzwords. What actually matters is whether those claims can be verified through clear, public, and independent facts. On that front, AequiSolva’s public disclosures raise serious questions.

AequiSolva’s biggest problem is not aggressive marketing, but overbuilt credibility theater

The most striking issue with AequiSolva is the way it uses language that sounds regulatory, sounds compliant, and sounds institutional, while stopping short of providing the kind of concrete information a genuinely transparent platform would normally disclose.

Instead of clearly telling the public which legal entity operates the platform, which licenses it holds, which regulators oversee it, and what registration numbers apply in each jurisdiction, AequiSolva leans heavily on a different strategy. It uses a dense combination of high-status regulatory terms and technical language to create the feeling that it already belongs inside a global compliance framework.

For many readers, this kind of presentation is highly persuasive. When people see SEC, CFTC, MiCA, MAS, SFC, and CSA mentioned together on one website, their first instinct is often not to ask whether the platform is actually licensed or merely describing itself as “aligned” with regulatory expectations. Their first instinct is to assume the platform must already be highly legitimate. That is exactly why this kind of writing is so effective. AequiSolva’s core issue is that it appears to be selling the atmosphere of regulation rather than providing the facts of regulation.

AequiSolva’s compliance narrative sounds strong, but that does not mean it is actually regulated

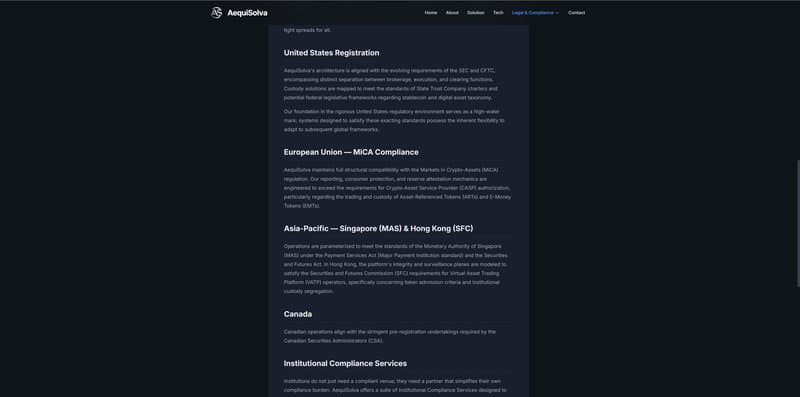

AequiSolva states on its website that its architecture is “aligned” with the evolving requirements of the SEC and CFTC, that its custody solutions are “mapped” to the standards of State Trust Company charters, that it maintains structural compatibility with the European Union’s MiCA framework, and that its operations are parameterized to meet regulatory standards in Singapore, Hong Kong, and Canada.

On the surface, that sounds like a platform built around major global regulatory systems. But the wording matters. AequiSolva uses phrases such as aligned with, mapped to meet, compatible with, parameterized to meet, and align with. It does not use the much more important and much more concrete language that would identify an actual regulatory status, such as licensed by, registered with, or authorized as.

That is not a minor wording difference. It is the entire difference. The first group of phrases describes the platform’s own internal narrative about how it sees itself. The second group would describe an actual legal and regulatory status that the public could independently verify. AequiSolva’s problem is not that it mentions regulation. Its problem is that it repeatedly borrows the authority of regulation without providing the basic information needed to confirm any real regulatory standing.

If AequiSolva wanted to prove its compliance story, it would make verification simple

Real compliance does not fear verification. A legitimately regulated business normally makes the verification process straightforward. The public should be able to identify the operating entity, check the relevant public register, review the license or registration status, and confirm the regulatory scope under which the business is allowed to operate.

AequiSolva does not make that process simple. Its website does not clearly present the exact regulated entities behind its claims, the relevant license numbers, the official registration identifiers, or even a full headquarters address. Instead, its contact page reportedly refers only to “United States” in a vague and incomplete way.

That is not transparency. That is omission. If a platform wants to wrap itself in the language of global compliance, then the burden is on that platform to provide the exact facts that allow the public to verify those claims. If the platform does not do that, then users are left with an impression instead of evidence.

Mentioning the SEC and CFTC is not the same as being regulated by the SEC or CFTC

The US-related language on AequiSolva’s website deserves especially close scrutiny. The platform appears to use phrases such as “our architecture is aligned with the evolving requirements of the SEC and CFTC” and “our foundation is built in the rigorous United States regulatory environment” in a way that encourages readers to associate the platform with serious US oversight.

But the obvious questions remain unanswered. Which exact legal entity is involved? What exact regulatory status does it hold? Who regulates it? Where can the public verify that relationship?

Those are not minor questions. They are the basic questions any serious platform should answer first.

This matters even more because the market has already seen cases where questionable operators exploit the prestige of US regulatory terminology to create a false sense of legitimacy. Many scam-related schemes do not directly say “we are fully licensed” if that claim would be easy to disprove. Instead, they rely on looser wording that sounds official enough to reassure inexperienced users while still giving themselves room to deny making a direct regulatory claim. AequiSolva’s wording fits that pattern uncomfortably well.

“Registered in the United States” sounds strong, but it means very little on its own

Another issue is the phrase “Registered in the United States,” which has reportedly appeared in promotional materials associated with AequiSolva. That statement may sound reassuring to ordinary readers, but in practical terms it is far too vague to establish credibility.

A US registration could mean many different things. It could refer to forming a company entity, filing a notice, maintaining a business record, or simply existing as a registered commercial entity in some state. None of those things automatically means a platform is regulated in the financial-services sense. None of them automatically means it is licensed to offer trading, custody, or investment-related services to the public.

For a platform that repeatedly invokes SEC, CFTC, State Trust Company standards, and the rigor of the US regulatory environment, falling back on a vague phrase like “Registered in the United States” is not a sign of strength. It is a sign that the platform may be more interested in borrowing authority than proving regulated status.

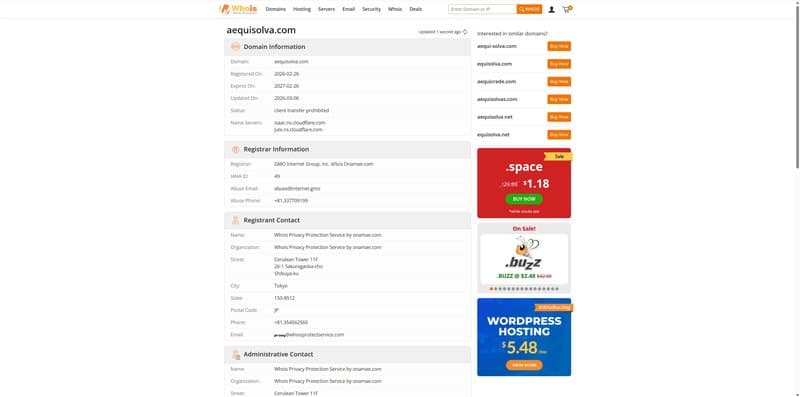

AequiSolva’s domain is extremely new, yet it presents itself like a long-established global platform

Another major red flag is the mismatch between AequiSolva’s public timeline and the maturity of its narrative. Whois records reportedly show that aequisolva.com was registered on February 28, 2026. At the same time, its visible brand footprint also appears to be very recent, with limited public presence and relatively little third-party visibility outside a narrow time window in late February and early March 2026.

That creates an obvious problem. AequiSolva does not present itself like a small early-stage website. It presents itself like a sophisticated, multi-jurisdictional, institution-facing financial system with prime brokerage ambitions, cross-asset margining, real-world asset integration, governance mechanics, and a full regulatory strategy.

That kind of mature positioning usually comes with a thicker public history. It usually leaves behind years of business traces, legal traces, leadership traces, product traces, and broader market recognition. AequiSolva, by contrast, appears to have built a very large story very quickly. That does not automatically prove fraud, but it is exactly the kind of mismatch that should make users stop and think.

The site looks more like a polished pitch package than a transparent operating platform

From a structural perspective, AequiSolva’s website looks more like a carefully designed financial concept presentation than a platform eager to expose its operating details to public scrutiny.

The homepage focuses on narrative: verifiable trust, regulatory leadership, asset fusion, layered architecture, ecosystem flywheel, roadmap, and AUSL governance. The contact page reportedly reads more like a business-development intake form, with categories such as Institutional Services, Partnership Opportunities, Technical Integration, Compliance & Regulatory, and Media & Press.

What is missing from the most visible public presentation is just as important as what is included. Clear legal-entity disclosure, a complete headquarters address, jurisdiction-by-jurisdiction operating boundaries, licensing details, and direct verification paths are not emphasized in the same way. When a platform constantly markets itself as verifiable, compliant, and institutional-grade, yet keeps its most basic corporate facts vague, that is not a small weakness. It is a serious credibility problem.

AequiSolva talks about “verifiable trust,” but does not make public verification clear enough

AequiSolva repeatedly tells users that it does not rely on “trust us” logic, but on “verify us” logic. It claims that through real-time Proof of Reserves and liability attestation, its solvency can be mathematically demonstrated at any block height, and that customer assets are segregated and protected from commingling risk.

This is powerful language because it touches the biggest fears in the crypto market: custody abuse, hidden liabilities, insolvency, and black-box operations. But if a platform truly wants to make verification central to its identity, then the most important thing it can do is place the verification tools directly in front of the public.

Where is the reserve verification page? What is the liability methodology? Who performs the attestation? What audit standards apply? Are historical records publicly accessible? Are the verification mechanisms independently reviewable?

If those answers are not clearly and prominently available, then the platform is not really handing verification over to the public. It is simply using the language of verification as part of its brand.

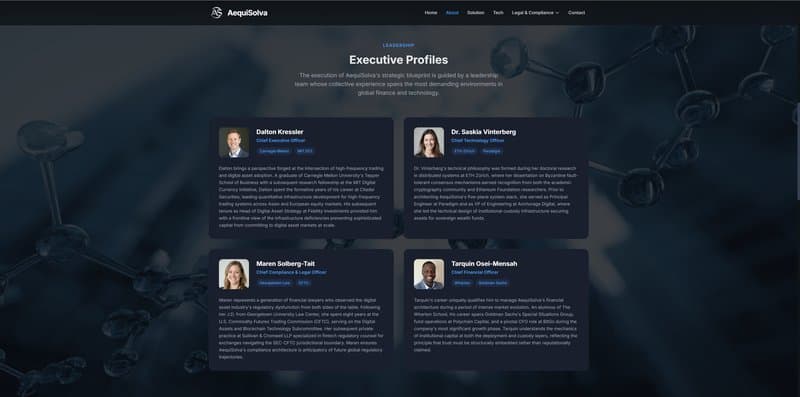

AequiSolva’s team narrative raises another major credibility concern

For any platform claiming to be global financial infrastructure, team credibility is critical. A company that genuinely has the capacity to align with major regulatory systems in the United States, the European Union, Singapore, Hong Kong, and Canada would normally have senior executives with visible professional histories.

A CEO, CTO, Chief Compliance Officer, and CFO operating at that level would usually leave some kind of public footprint through professional profiles, prior employment records, conference appearances, media interviews, legal records, or industry references. According to the concerns raised here, however, AequiSolva’s publicly presented team members appear to be extremely difficult to verify online, with no meaningful LinkedIn trail and no obvious independent public background.

One missing profile might mean nothing. Two unclear names might still be coincidence. But if an entire executive team cannot be meaningfully verified through normal public searches, that becomes highly suspicious. It raises a serious question about whether the people presented on the site are real, accurately described, or even genuinely connected to the platform at all.

AequiSolva’s media coverage looks more like PR distribution than independent validation

Externally, AequiSolva appears to be building media visibility quickly, but that is not the same thing as building trust. One of its more visible outside mentions is a March 3, 2026 article reposted on MEXC News about AequiSolva deploying institutional-grade MPC architecture for digital asset security. The article references cold storage, SOC monitoring, 2FA, whitelisting, and cryptographic security, while again using the phrase “Registered in the United States.”

The problem is that this kind of media presence does not necessarily indicate independent validation. If the article is ultimately a distributed promotional piece rather than a critical or investigative third-party review, then what readers are seeing is not real market confirmation. They are seeing a brand narrative moving through a distribution chain.

In the crypto space, being republished is not the same as being verified. Being mentioned is not the same as being endorsed. If a platform’s outside visibility relies more on promotional-style coverage than on transparent regulatory, audit, licensing, or long-term operational records, that visibility should be treated with caution rather than confidence.

Why AequiSolva looks highly suspicious

When all of these points are considered together, AequiSolva’s risk profile becomes much clearer. On one hand, it repeatedly uses the language of SEC, CFTC, MiCA, MAS, SFC, and CSA to create the impression of a deeply compliant platform. On the other hand, it does not provide equally clear, equally direct, and equally easy-to-verify regulatory identity information.

It presents itself as an institutional-grade, multi-jurisdictional, future-facing financial infrastructure platform, yet its public footprint is extremely new and its website feels more narrative-driven than transparency-driven. It markets “verifiable trust,” yet does not make public verification tools the most obvious part of its presentation. It has media mentions, but they look closer to brand distribution than to independent validation. And its executive narrative appears unusually difficult to verify.

For ordinary users, the danger is not just one isolated issue. The real danger is the overall pattern. AequiSolva does not look like a platform that has already earned trust through established facts. It looks far more like a platform trying to manufacture trust in advance through terminology, structure, imagery, and presentation.

Conclusion

So, is AequiSolva a scam?

Based on the publicly reviewable information available at this stage, the more careful and responsible conclusion is that AequiSolva is at least a highly questionable platform with multiple serious red flags. Its biggest weakness is not that it lacks ambition. Its biggest weakness is that its story is far bigger, more polished, and more institutional-looking than the verifiable facts currently available to the public.

A genuinely trustworthy platform does not need to keep repeating that it is ready for global regulatory frameworks. It answers the simple questions first: Who operates it? Who regulates it? Where is it licensed? Where can users verify that? Who audits it? Who independently confirms its claims?

Until AequiSolva provides clear answers to those questions, it is difficult to view the platform as mature, credible, or well-supported by solid regulatory foundations. The more accurate description is that AequiSolva appears to be staging trust rather than proving it.