DIVEXA, also known as Divexa Exchange, claims to be a global digital asset trading platform tailored for the Web3 era. It markets itself with “smart trading,” “derivatives trading,” and “one-stop services,” repeatedly emphasizing its MSB registration in the U.S. and Form D filing, giving the appearance of a somewhat “compliant” crypto platform. Many investors dropped their guard due to these professional terms and the “U.S. registered company” label, subsequently pouring in their funds.

This article will not promote DIVEXA but will dismantle this platform piece by piece based on public information and third-party investigations. We will examine its so-called “compliance qualifications,” website and product design, information disclosure, and real user risk points to see whether it is truly safe and reliable or a high-risk trap disguised in compliance clothing, helping investors discern its true nature before taking action.

Is DIVEXA a legitimate platform?

To conclude: despite DIVEXA’s promotion as a "Web3 era global digital asset platform" claiming "compliance" and "security intelligence," current public information suggests a multitude of high-risk signals from this platform. For ordinary investors, it seems more like a carefully packaged scheme rather than a reliable exchange.

Extravagant promotions on the official website and "data site"

If you only view the DIVEXA sites, it looks like this:

- Claiming to be a "global digital asset trading platform built for the Web3 era", providing one-stop services including spot, contract, options, and yield products;

- Constantly emphasizing "bank-level security architecture, cold and hot wallet separation, real-time risk control monitoring, Proof of Reserves, strict compliance";

- Public address uniformly pointing to an office building in Jersey City, New Jersey, USA;

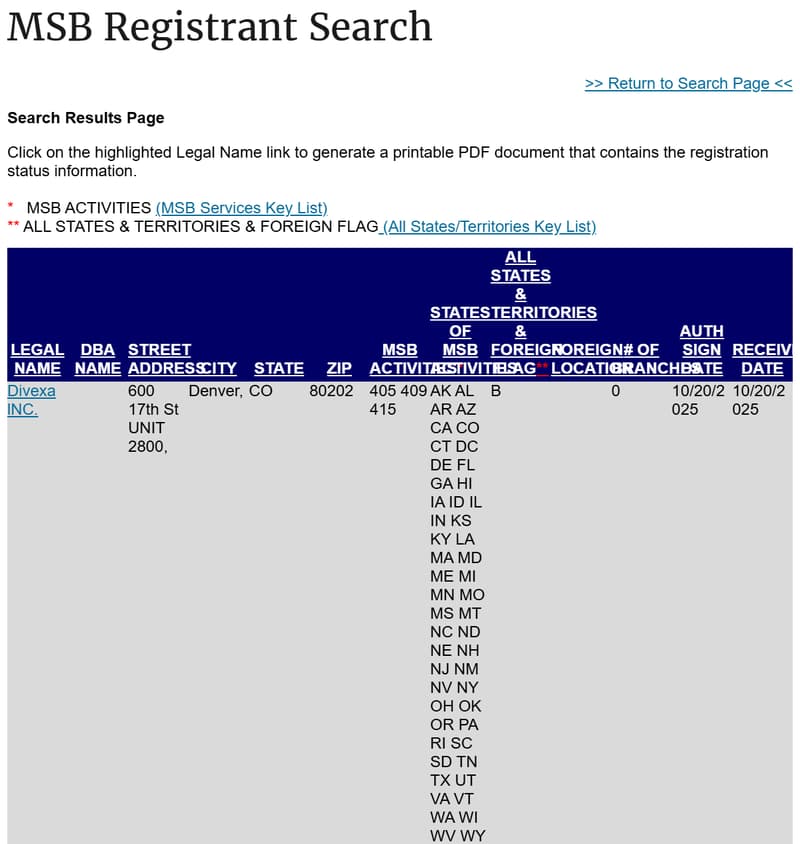

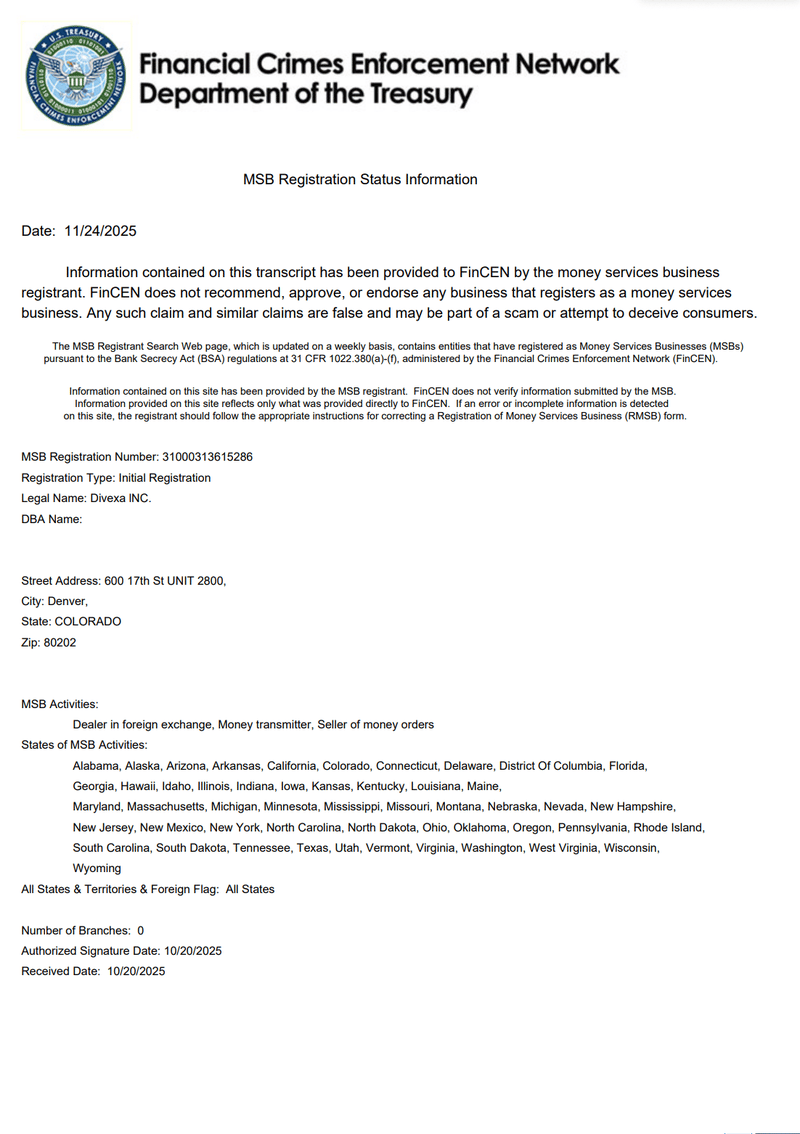

- Repeatedly mentioning its registration with FinCEN as an MSB, submission of Form D under Reg D to the SEC, and records with the Colorado Secretary of State.

On the surface, it looks like a “U.S. licensed institution + high-tech Web3 exchange.” This is where many let their guard down.

The problem is—if these labels are not scrutinized separately, they can easily become "fake regulatory rhetoric."

MSB and Form D, repeatedly touted as "compliance qualifications," do they truly protect investors?

FinCEN MSB: Merely an “anti-money laundering registration,” not a trading license

DIVEXA indeed has relevant registration information in the FinCEN MSB registry, indicating it has been filed as a Money Services Business.

The crucial point is: FinCEN itself makes it clear on the MSB search page—listing an institution in the MSB registry does not mean that any government agency recommends, certifies its legality, or endorses it.

The essence of MSB is:

- Primarily revolves around anti-money laundering, fund transfers, and basic compliance processes;

- Typical businesses include currency exchange, remittances, prepaid cards, traveler’s checks, etc.;FinCEN.gov+1

- Not equivalent to "allowing you to engage in global crypto futures, options, and derivatives trading."

In other words: MSB is more like informing regulators "I am providing financial services here, please monitor me for anti-money laundering," rather than "I have obtained a legitimate crypto derivatives brand license."

If a platform packages "FinCEN MSB registration" as a "U.S. federal strong regulatory endorsement," it is either severely lacking professionalism or intentionally misleading.

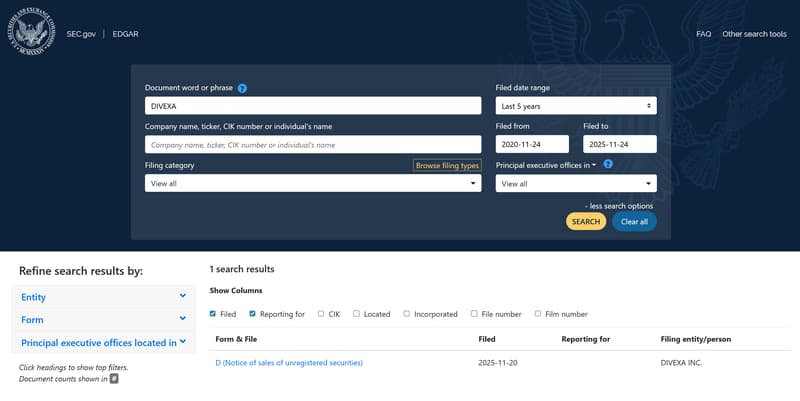

SEC Form D: A “notice of exemption issuance,” not any form of “approval”

In the SEC’s EDGAR system, Form D documents for DIVEXA INC. can be found—a notice of exempt securities issuance under Reg D.

According to SEC and Investor.gov,:

- Form D is just a “short notification” a company submits to the SEC when relying on Reg D exemption to issue securities;

- Such exempt issuances bypass the traditional public offering registration process, regulators do not conduct in-depth scrutiny of business models or profit forecasts;

- More importantly: Form D is a self-report of "We sell private placement securities and claim to comply with exemption conditions," not "The SEC has reviewed and approved this project."

Many compliance articles have repeatedly emphasized—considering Form D as “SEC certification” is a misconception, even directly naming: Form D is a notice, not an endorsement.

If a platform promotes “we are registered with the SEC, so we are safe,” it can basically be labeled as "marketing over substantive regulation."

Does DIVEXA's claimed business align with its licenses?

According to DIVEXA, it engages in:

- Crypto spot trading for global users;

- Crypto futures, options, and other high-leverage derivatives;

- Structured return products, Web3 tools, etc.

However, the compliance licenses/registrations they publicly present mainly include:

- FinCEN MSB registration (focus on anti-money laundering & fund services);

- Form D notification under the Reg D framework for private security issuance;

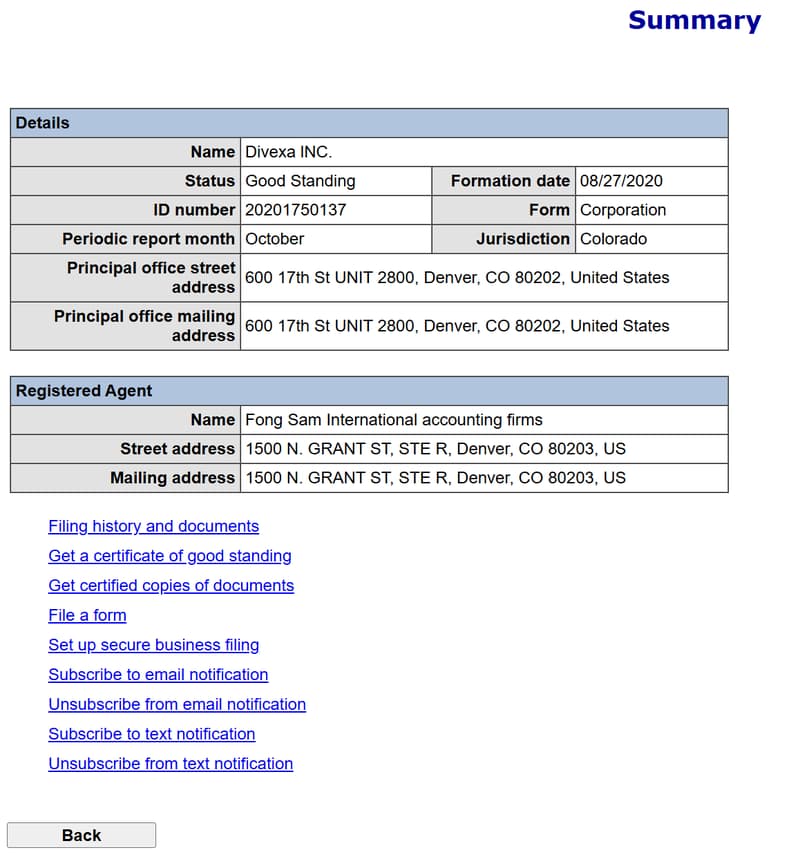

- State-level ordinary business registration (e.g., Colorado Secretary of State).

These alone are miles away from being a “crypto derivatives exchange regulated under securities/futures licences”—you can’t see:

- Any clear license categories (such as which securities/futures/virtual asset service provider regulations they align with);

- Any specific license number, issuing authority link, applicable jurisdiction statement;

- Which regulatory body explicitly includes “crypto contract trading” as a regulated activity within license permissions.

TraderKnows, in its risk rating of DIVEXA, has directly categorized this type of MSB+Form D combination as a "fake regulation," marking its status as Scam and assigning it the industry’s lowest E-grade.

From an investor’s perspective, this seems more like piecing together "every official term you can write on a website" to create an impressive "compliance story," but actually little that truly protects you.

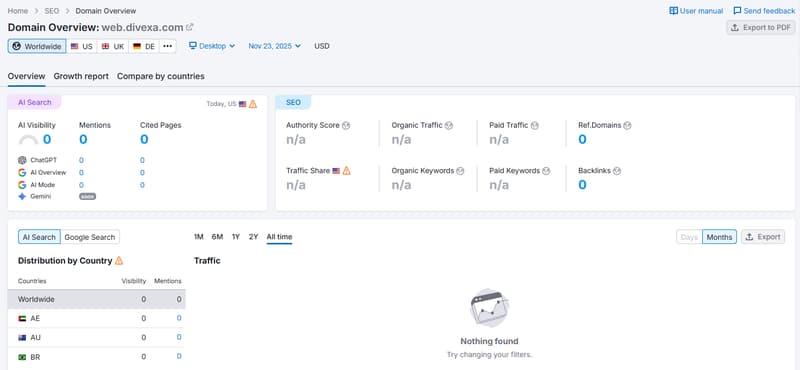

Old domain, lack of traffic, and absent social media: a “platform without users”

Now let’s look at its online presence:

- The domain divexa.com was registered on 2015-08-01, looking like an “old domain”;

- But data from TraderKnows based on Semrush crawls show web.divexa.com had nearly no organic traffic, keyword rankings, backlinks, or visits during evaluation, essentially "invisible" on search engines.

- The official contact only left a [email protected] email, without visible and transparent social media presence (main Twitter, Telegram, LinkedIn, Instagram lacking or having almost no real interaction).

Meanwhile, DIVEXA is frequently mentioned across news distribution sites and PR platforms—FinanceWire, GlobeNewswire, 24-7PressRelease, Benzinga, with announcements of "cross-chain tool upgrades," "matchmaking engine updates," and "institutional liquidity centers."

This contrast is quite telling:

Real exchange: User communities, complaints, discussions, developer ecosystems abound, while PR draft is merely supplementary.

Problematic platform: PR drafts everywhere, a search returns almost entirely their own or partner praise, with real user voices rare or negative.

On YouTube, there are videos dedicated to warning against DIVEXA, highlighting issues with withdrawal obstacles, false promises, and unlicensed operations.

Although these videos are not official investigations, they at least indicate a fact: DIVEXA’s reputation among real users is far from the perfection depicted in their press releases.

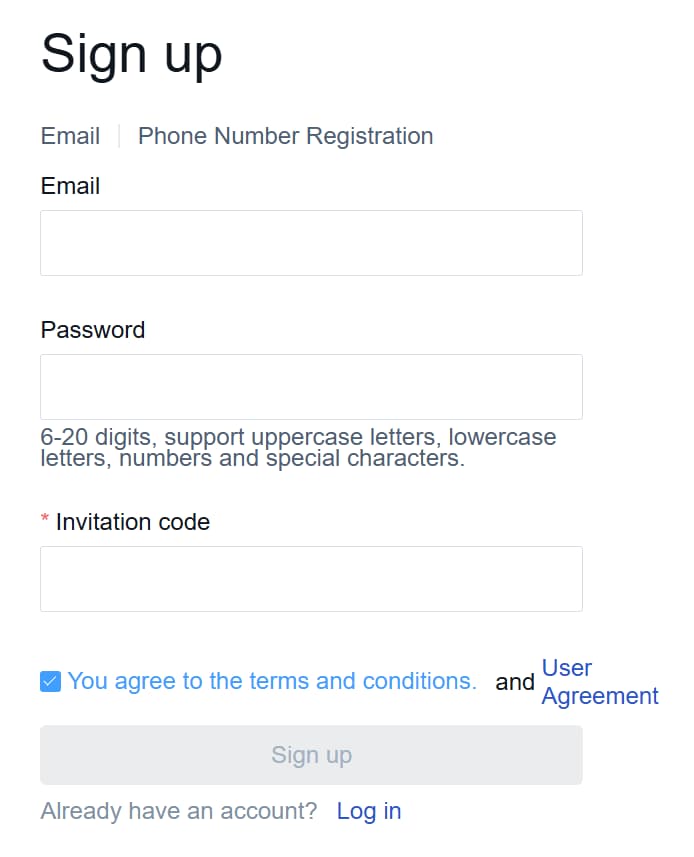

Website details: Smooth registration, vague information

Back to the platform itself. TraderKnows’ site experience reveals:

- Registration is extremely smooth: Minimalist forms, clear fields, instant error prompts, very friendly to beginners;

- Product introduction is vague: Contracts and options are clearly mentioned, yet there is almost no detailed contract rules, clearance mechanisms, forced liquidation logic, or fee rate details;

- Account types and trading conditions are not transparent: No publicly available information on different account thresholds, spread/fee structures, leverage caps, etc.;

- Lack of education section: No beginners' guides, risk alerts, or strategy tutorials, quite unfriendly to those new to crypto derivatives;

- Flat website structure, messy navigation: Key information scattered in various corners, requiring back-and-forth navigation to piece together any full picture.

The ironic part is:

Your path for "opening an account + depositing funds" is designed to be smooth and frictionless;

Whereas content crucial to understanding risks and rules requires painstaking effort to "dig out."

This is not the attitude of a responsible trading platform.

Third-party "whitewashing info site": self-proclaimed “legitimate and long-term faction”

It's noteworthy that there is a dedicated "Divexa wiki/info site" online that attempts to package DIVEXA as a “structure clear, compliance framework clear, long-term belief” legitimate platform:

- Emphasizing "bank-level security, security system, Proof of Reserves, education-oriented";

- Describing "FinCEN MSB registration + Reg D framework" as "more transparent and compliant than anonymous platforms";

But if you compare these “whitewash articles” with official PR, you’ll find highly consistent rhetoric:

- The same repetition of keywords: security, intelligence, one-stop, global, multiple licenses;

- Avoidance of specific regulatory numbers, specific business jurisdiction scope;

- Not mentioning any real user disputes or reputation controversies.

This type of content seems more like a "content matrix" from the same PR team, rather than an independent third party performing user-standpoint scrutiny.

Why is DIVEXA a "high-risk platform" rather than just a "new platform"?

Based on currently available information, DIVEXA exhibits at least these typical high-risk characteristics:

- Using registration to masquerade as licenses and blurring procedural compliance into “strong regulation”

- Presenting FinCEN MSB registration, Reg D Form D as evidence of being "under U.S. regulation";

- With both official and "info site" stress on "compliance framework" and "multiple jurisdiction licenses alignment," yet never outright stating if they have any real regulatory permissions for crypto derivatives business.

- Presenting FinCEN MSB registration, Reg D Form D as evidence of being "under U.S. regulation";

- Severe imbalance in information disclosure

- Heavily emphasizes deposit and trading features;

- Unable to see comprehensive public documentation of trading rules, risk control mechanisms, fee structure, and account rights protection.

- Heavily emphasizes deposit and trading features;

- Anomalous traffic structure

- The domain is not young, but with almost zero organic traffic and weight;

- External exposure primarily relies on large-scale press releases rather than organic community discussions and user-generate content.

- The domain is not young, but with almost zero organic traffic and weight;

From an ordinary investor’s perspective, there is almost no substantial evidence to trust it, yet it is easy to find many unfavorable clues. This alone is enough to classify it as a “platform to avoid.”

If you've already been involved with DIVEXA, here are some steps to take

If you have already opened an account with DIVEXA or have funds in it, consider at least taking these precautionary steps:

Try to withdraw all funds

- Attempt small and multiple withdrawals;

- Keep all screenshots, email communications, blockchain transaction records;

- If confronted with excuses for delays or demands for "tax payment," “unfreezing fund,” “raising level to withdraw,” consider it a major red flag.

Verify "regulatory licenses" claimed by the official

Consider a straightforward three-step verification approach (TraderKnows article also mentions similar methods):

- Check DIVEXA INC’s company information on the Colorado Secretary of State website to see if it truly exists and its status;

- Use the declared registration number to query on FinCEN’s MSB search page, confirming registration status and whether business types cover its publicly claimed business;

- Check Form D original text in SEC's EDGAR system, noting fundraising targets, amounts, issuance nature, and not be misled by "having Form D."

You will find: even if these records exist, it does not mean that the platform has the qualification to conduct global crypto contract trading for retail investors.

Diversify risk, do not tie holdings to one suspicious platform

- Whenever possible, move long-term held coins and valuable assets to wallets where you control the private key or reputable compliant platforms;

- Do not believe in any “internal channels,” “custodial income,” “guaranteed high interest” for secondary redirection.

Final note: Don’t be fooled by those “compliance terms”

The most dangerous aspect of platforms like DIVEXA is not an unattractive UI or system lags, but its exploitation of “grey areas” within regulatory systems:

- Packaging FinCEN MSB registration as “U.S. Treasury regulation”;

- Misrepresenting Form D as “SEC-approved document”;

- Using a plethora of sophisticated compliance and technical terminology to obscure the core issue—

Who is truly responsible for your money once it’s in? Which veritable regulatory body will you find should issues arise?

If a platform truly aims for long-term presence, it wouldn't tolerate itself being almost unsearchable in natural rankings, solely relying on numerous press releases for visibility, nor would it evade clear disclosure of license information and business boundaries.