97EX is a digital asset brokerage company with an undisclosed founding date, claiming registration in Wyoming, USA, and headquartered in Cheyenne. It offers various trading options such as cryptocurrency spot, high-leverage contracts, OTC, custody, and lending. The platform provides basic educational resources and supports multiple languages. It uses a self-developed web and mobile trading platform with tiered account fees; the minimum deposit is not specified, and the contract leverage limit is unmentioned with funding rates adjusting with the market.

Regulation and Qualifications: Nominal Registration ≠ Regulation

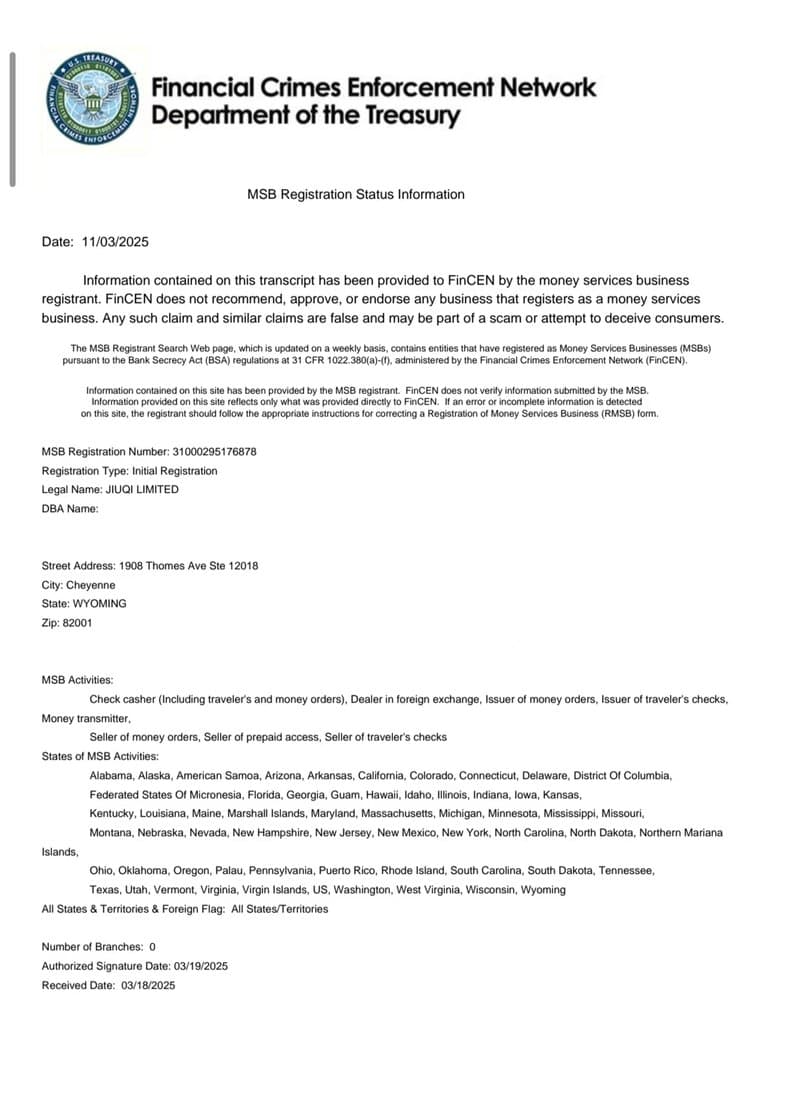

- The public entity is JIUQILIMITED, registered with FinCEN as an MSB, but the registered business activities focus on traditional finance like currency exchange/fund transfer, which does not equate to a license for crypto assets or securities operations.

- FinCEN's document explicitly states that "registration does not constitute approval or endorsement," and promoting "FinCEN approval" is misleading.

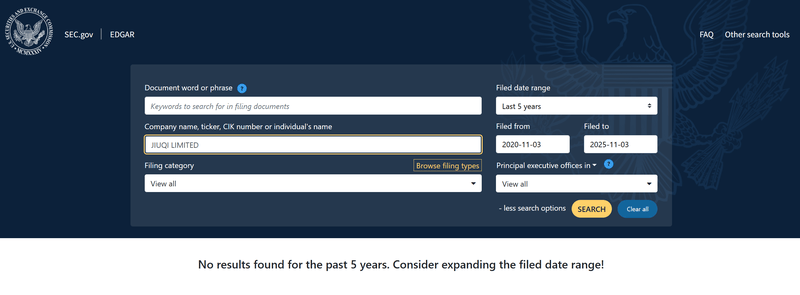

- No valid filings for "97EX" or "JIUQILIMITED" were found on the SEC Edgar database. Engaging in securities or securitized digital asset-related businesses within the U.S. typically requires higher-level compliance authorizations.

Conclusion: There is a significant regulatory gap, with compliance narratives not matching actual authorizations.

Domain and Brand: Old Shell for New Use, Timeline Doesn't Prove Credibility

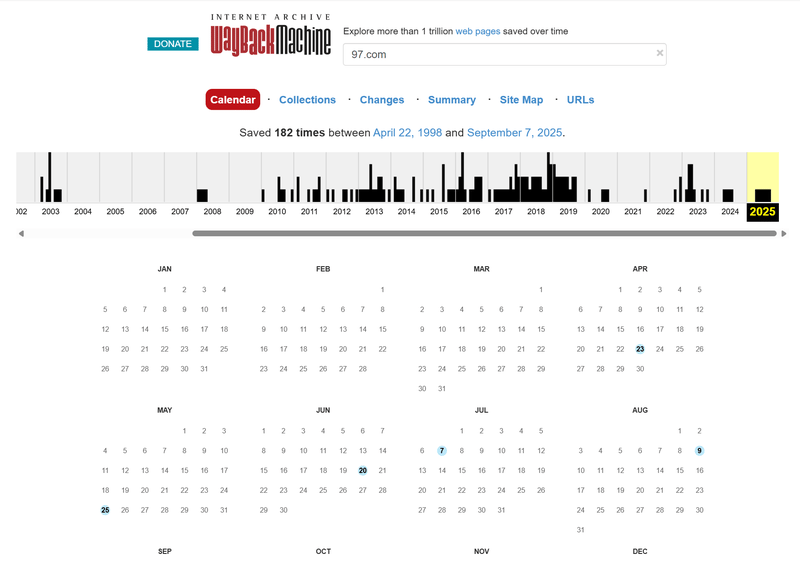

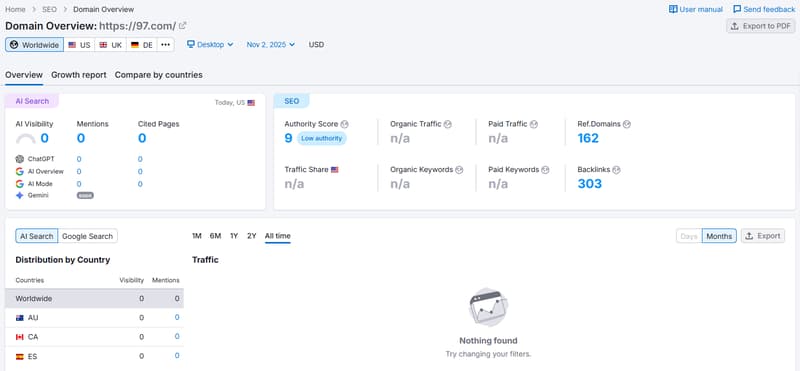

- The main domain 97.com has been registered for a long time, but a strong association with the "97EX" brand has only formed in the past two years; historical snapshots indicate it was dormant for a long period before being reactivated.

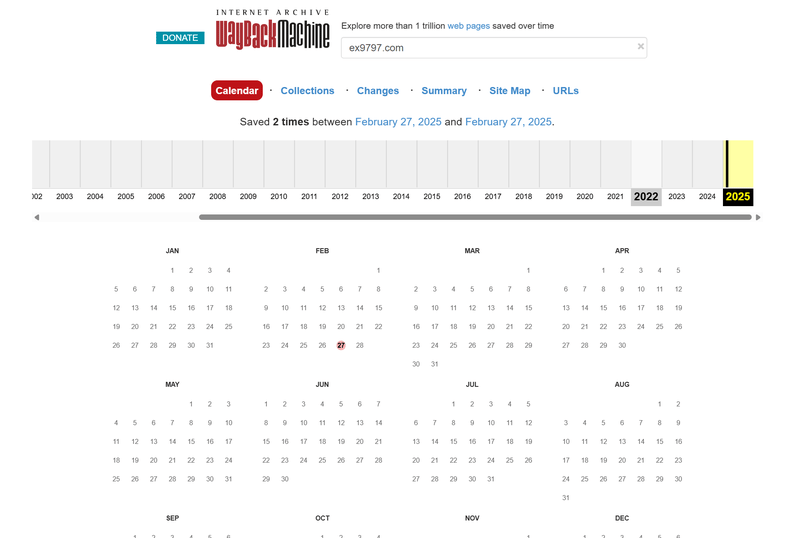

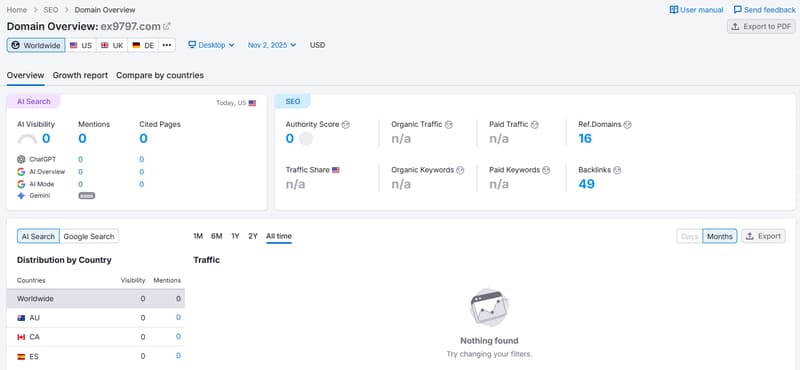

- The promotional domain ex9797.com was registered on February 26, 2025, using privacy protection, targeting more towards attracting and guiding the Chinese market.

Conclusion: This is a typical "old domain + new project" combination, where domain age does not equate to platform maturity and risk control capability.

Overextended Business Scope: From Spot, Contracts to Custody Loans and "Stock OTC"

- The official scope includes spot, perpetual high-leverage, OTC, custody, and lending, even touching on "stocks".

- Such broad product lines usually require more complex licensing chains in heavily regulated jurisdictions; when no corresponding authorization is found in SEC and other public databases, the more products, the greater the potential compliance mismatch.

Conclusion: The business extension is disproportionate to licensed scope, compounded by counterparty risk and liquidation risk.

Agency and Commission: High Percentage Multi-Level Structure of 30%–45%

- Commissions are tiered based on monthly trading volume: 30%/35%/40%/45%.

- High commissions and multi-level structures are historically aligned with "volume for voice" driven growth; once genuine users and transactions are insufficient, platforms often shift to a "fee-driven" consumption model.

Conclusion: The strong incentivization structure exacerbates traffic-related risk, likely enticing high-frequency and high-leverage activities.

Weak External Signals: Near Zero Traffic, Minimal Social Media Updates

- Semrush estimates for the two associated domains show zero visitors; except for Telegram, there is virtually no effective update or interaction on multiple social media platforms.

Conclusion: Lacking genuine user volume and third-party word-of-mouth validation, the narrative of "global operations" is hard to substantiate.

Product Experience and Customer Service: Entrances are Confused, Links are Fragile, Email-Only Support

- The website's navigation has shallow levels, unclear categorization, and some unstable links; the logic of registration and trading entries is not intuitive.

- Customer service is primarily via email, with common response times ranging from 24–48 hours, using "submission for review" when dealing with delays in funds/technical issues.

Conclusion: In high-sensitivity businesses related to funds, single and lagged customer service forms struggle to effectively manage pressure.

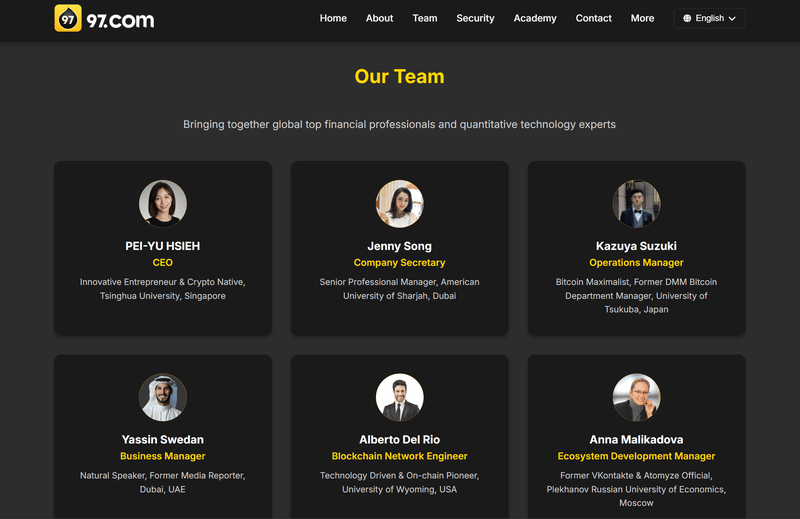

Team Presentation Lacks Verifiable Anchors

The page lists names of "executives/technology/marketing" but generally lacks verifiable credentials, licenses, or links to third-party endorsements.

Conclusion: Relying solely on self-reported names fails to form a credible character circle.

Customized Self-Check List

- SEC Edgar Verification: Simultaneously search "97EX" and "JIUQILIMITED," focusing on Form D/Reg D, etc.

- FinCEN Registration: Compare registered business types with the platform's actual products, remembering "registration ≠ license."

- Domain and Snapshots: Review 97.com and ex9797.com's Whois and Wayback Machine timelines to identify "new uses of old domains."

- Trading Rules Traceability: Capture and archive images of forced liquidation levels, funding rates, leverage limits, and risk management parameters; note if page statements are consistent.

- Blockchain Path Sampling: If public heat wallet addresses are claimed, sample check incoming and outgoing transactions and aggregation logic.

- Agency Agreement Terms: Define commission sources, settlement criteria, risk control trigger conditions, and appeal paths.

- Customer Service Evidence Chain: Retain all ticket and email correspondence timestamps, record screen if necessary.

Risk Assessment

- Regulatory Risk: High—FinCEN registration does not equal crypto/securities license, absent SEC Edgar filings.

- Operational Risk: Medium-High—Multiple products combined with rules that need confirmation; entry and link stability is poor.

- Counterparty Risk: Medium-High—High commission newcomer structures coexisting with low external volume.

- Information Transparency: Medium-Low—Weak verifiability of the team, missing social media and third-party data.

Overall Conclusion: 97EX exhibits several high-risk characteristics, and it is not recommended to consider it as a compliant and reliable trading partner. For those with limited risk tolerance, staying away from this platform is more prudent.